Choosing the right Health Insurance Company is a critical decision that can significantly impact your financial security and access to quality healthcare. With numerous options available, it’s essential to evaluate various factors to ensure you select a plan that aligns with your health needs, budget, and personal circumstances.

Key Takeaways

- Assess Personal Health Needs: Health Insurance Company Understand your medical requirements to choose appropriate coverage.

- Evaluate Insurer’s Reliability: Consider factors like CSR and customer reviews.

- Understand Policy Terms: Be aware of waiting periods, co-payment clauses, and exclusions.

- Compare Multiple Policies: Don’t settle for the first option; compare various plans to find the best fit.

- Review Regularly: Periodically reassess your policy to ensure it continues to meet your needs.

Understanding Health Insurance

Health Insurance Company is a contract between you and an insurer that provides financial coverage for medical expenses. It typically covers hospitalization costs, surgeries, doctor visits, and sometimes preventive care. In return, you pay a monthly premium, and the insurer covers a portion of your medical expenses.

Key Factors to Consider When Choosing a Health Insurance Company

- Assess Your Healthcare Needs Begin by evaluating your Health Insurance Company status and that of your family members. Consider factors such as:

- Chronic conditions: Do you or any family member have ongoing health issues?Age: Older individuals may require more frequent medical attention.Lifestyle: Active individuals might need coverage for sports-related injuries.Family planning: If you plan to start a family, maternity coverage becomes essential.

- Evaluate the Claim Settlement Ratio (CSR) The CSR indicates the percentage of claims an insurer settles out of the total claims received. A higher CSR suggests efficient claim processing and reliability. For instance, a CSR of 95% means the insurer settles 95 out of 100 claims.

- Check Network Hospitals Ensure the insurer has a wide network of hospitals, especially those near your residence. A broad network facilitates cashless treatment, reducing out-of-pocket expenses during hospitalization.

- Understand the Waiting Periods Health insurance policies often have waiting periods for pre-existing diseases, maternity benefits, and specific treatments. Opt for policies with shorter waiting periods to ensure timely coverage.

- Review the Co-payment Clause Some policies require you to bear a percentage of the claim amount, known as co-payment. While this can reduce premiums, ensure you can afford the out-of-pocket expenses during a medical emergency.

- Consider the Sum Insured The sum insured is the maximum amount the insurer will pay for medical expenses. Choose a sum insured that adequately covers potential medical costs, considering inflation and rising healthcare expenses.

- Look for Additional Benefits Many insurers offer added benefits like:

- No-Claim Bonus (NCB): A discount on premiums for claim-free years.

- Free Health Check-ups: Regular health assessments.

- Maternity and Newborn Cover: Coverage for childbirth and related expenses.

- Daycare Procedures: Health Insurance Company Coverage for treatments that don’t require 24-hour hospitalization.

- Compare Premiums While it’s tempting to choose the cheapest option, ensure the policy offers comprehensive coverage. Sometimes, paying a slightly higher premium can provide better benefits and broader coverage.

Understanding Policy Exclusions

Every health insurance policy comes with a set of exclusions—conditions or treatments that are not covered under the policy. It’s crucial to thoroughly review these exclusions before purchasing a plan. Common exclusions may include:

- Cosmetic surgeries

- Pre-existing conditions during the waiting period

- Certain types of dental or vision care

- Alternative treatments not recognized by the insurer

Understanding these exclusions helps in setting realistic expectations and avoiding surprises during claim settlements.

The Role of Customer Service

Efficient customer service is vital when dealing with Health Insurance Company. A responsive and helpful customer service team can assist in:

- Clarifying policy details

- Guiding you through the claim process

- Addressing grievances or concerns promptly

Before finalizing your choice, assess the insurer’s customer service reputation. Look for reviews and ratings to gauge their Health Insurance Company responsiveness and effectiveness.

Impact of Lifestyle Changes on Health Insurance Needs

Life events such as marriage, the birth of a child, or the onset of a chronic illness can significantly impact your health insurance needs. It’s essential to:

- Review and adjust your coverage to accommodate new family members or health conditions.

- Consider adding riders or additional coverage for maternity, critical illness, or personal accident benefits.

- Update your insurer about any significant lifestyle changes to ensure continuous and adequate coverage.

Importance of Preventive Healthcare Coverage

Preventive care, including regular check-ups, vaccinations, and screenings, plays a crucial role in maintaining health and detecting potential issues early. Some health insurance plans offer:

- Annual health check-ups

- Vaccination coverage

- Discounts on wellness programs

Opting for a plan that includes preventive care can lead to long-term health benefits and cost savings.

Understanding the Terms of Renewal

Health Insurance Company are typically renewable annually. However, it’s essential to understand the terms of renewal, including:

- Age limits: Some policies may have age restrictions for renewal.

- Premium increases: Premiums may rise with age or due to claim history.

- Policy modifications: Insurers may alter terms or conditions upon renewal.

Clarifying these aspects ensures that you won’t face unexpected challenges during policy renewal.

Evaluating Insurer’s Financial Stability

The financial health of an Health Insurance Company indicates its ability to pay claims. Before choosing an insurer, consider:

- Credit ratings: Agencies like ICRA, CRISIL, and CARE Ratings provide insights into an insurer’s financial stability.

- Claim settlement ratio: A higher ratio suggests efficient claim processing.

- Regulatory compliance: Ensure the insurer adheres to guidelines set by the Insurance Regulatory and Development Authority of India (IRDAI).

Exploring Group Health Insurance Options

If you’re employed, your employer may offer group Health Insurance Company. While these plans can be cost-effective, they may have limitations:

- Coverage limits: Group plans may offer lower coverage amounts.

- Portability: Coverage may end upon leaving the job.

- Customization: Limited options to tailor the plan to individual needs.

Assess whether supplementing a group plan with an individual policy is beneficial.

Considering International Health Insurance

If you travel frequently or reside abroad, international Health Insurance Company may be necessary. These plans offer:

- Global coverage: Access to healthcare services worldwide.

- Emergency evacuation: Health Insurance Company Coverage for medical emergencies requiring transportation.

- Repatriation: Assistance in returning to your home country for treatment.

Ensure that the plan meets the healthcare standards of the countries you visit or reside in.

Utilizing Technology for Comparison

| Technology Tool / Feature | Description | Benefits | Example Platforms |

|---|---|---|---|

| Online Comparison Websites | Health Insurance Company Websites that aggregate and display multiple insurance plans side-by-side based on user input. | Easy, quick overview of premiums, benefits, and exclusions. | PolicyBazaar, Coverfox, GoHealthIndia |

| Mobile Apps | Insurer or aggregator apps allowing you to browse, compare, and buy policies on the go. | Convenience of managing Health Insurance Company from smartphone; instant quotes and document access. | ICICI Lombard app, Max Bupa app |

| AI Chatbots & Virtual Assistants | Bots that answer Health Insurance Company queries, guide plan selection, and explain terms interactively. | 24/7 support, personalized recommendations based on your needs. | HDFC Ergo chatbot, Tata AIA bot |

| Customer Reviews & Ratings Portals | Websites/apps showing real customer feedback and insurer ratings. | Insight into service quality, claims experience, and trustworthiness. | MouthShut, Trustpilot, Google Reviews |

| Claim Settlement Trackers | Platforms that track insurer claim settlement ratios and speed. | Helps evaluate insurer reliability and efficiency in claim processing. | IRDAI’s official website, Insurance Company portals |

| Premium Calculators | Interactive tools where you enter personal and health details to estimate premiums instantly. | Provides personalized premium estimates for better budgeting. | PolicyBazaar premium calculator, insurer websites |

| Comparison APIs for Developers | APIs that integrate insurance data into third-party apps or websites for custom comparison tools. | Enables customized insurance comparison experiences. | To be integrated by startups or fintech apps |

| Document Upload & Verification Tech | Tech that allows scanning and uploading documents for faster claim processing and application. | Speeds up paperwork, reduces errors, and improves claim approval rates. | Insurer mobile apps, third-party platforms |

Several online platforms allow you to compare health insurance plans based on:

- Premiums

- Coverage

- Insurer ratings

- Customer reviews

Utilizing these tools can help you make an informed decision by providing a side-by-side comparison of available options.

Seeking Professional Advice

If you’re overwhelmed by the choices, consider consulting with an insurance advisor. They can:

- Assess your needs: Understand your health requirements and financial situation.

- Recommend suitable plans: Suggest policies that align with your needs.

- Assist with paperwork: Help in filling out applications and understanding terms.

Ensure that the advisor is licensed and has a good reputation.

Analyzing Different Types of Health Insurance Plans

Health Insurance Company comes in multiple plan types, each designed for specific needs and preferences. Understanding these options will help you choose a policy from the right Health Insurance Company that matches your expectations.

Indemnity Plans (Reimbursement Plans)

- You pay for medical treatment upfront.

- Submit claims to the insurer for reimbursement.

- Usually offers broad coverage but may require more paperwork.

Managed Care Plans

Includes Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), and Point of Service (POS) plans.

- HMOs: Require choosing doctors and hospitals within the network; need referrals for specialists.

- PPOs: More flexibility to see any healthcare provider; higher premiums and deductibles.

- POS: Hybrid of HMO and PPO, with network flexibility but referrals required.

High Deductible Health Plans (HDHPs)

- Lower monthly premiums but higher deductibles.

- Often paired with Health Savings Accounts (HSAs) for tax benefits.

- Suitable if you’re generally healthy and want lower premiums.

Understanding Premiums, Deductibles, and Out-of-Pocket Maximums

These three factors influence how much you pay overall.

- Premium: Regular payment (monthly or yearly) for maintaining coverage.

- Deductible: Amount you pay out of pocket before insurance starts covering costs.

- Out-of-Pocket Maximum: Maximum you pay in a year; after this, insurance covers 100%.

When choosing a company, compare how these costs balance out. A company offering competitive premiums but very high deductibles might not be best if you expect frequent Health Insurance Company needs.

Reading and Interpreting the Fine Print

Health Insurance Company policies contain terms, conditions, and clauses that affect your coverage.

- Pre-existing condition clauses: Some insurers may exclude coverage or impose longer waiting periods.

- Renewability terms: Check if the insurer offers lifetime renewability.

- Coverage limits: Health Insurance Company policies have caps on room rent, treatments, or certain diseases.

- Sub-limits on treatments: Important to understand limits on ICU charges, day care procedures, or diagnostics.

Thoroughly reviewing policy documents ensures there are no unpleasant surprises during claims.

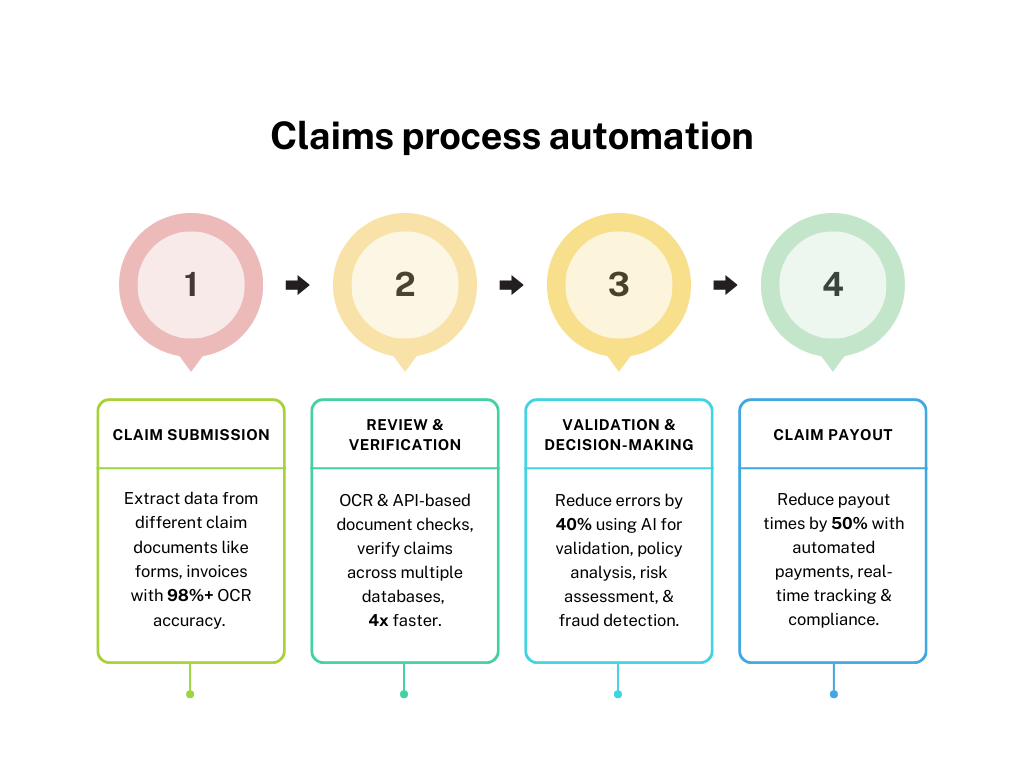

Evaluating the Claims Process

Even the best policy is useless if the claims process is cumbersome.

- Research how quickly the insurer settles claims.

- Understand the documentation required.

- Check if they offer cashless hospitalization facilities.

- Look for availability of 24/7 claims support.

You can gauge this by reading customer reviews and checking independent ratings.

Health Insurance Riders: Customize Your Policy

Riders are additional benefits you can add to your base health insurance policy for enhanced coverage.

Common riders include:

- Critical illness rider: Covers specific diseases like cancer, heart attack, etc.

- Maternity rider: Covers pregnancy and childbirth expenses.

- Personal accident rider: Provides coverage for accidents leading to disability.

- Hospital cash rider: Daily cash allowance for hospitalization.

Choosing a company that offers flexible riders lets you tailor the policy as per your individual or family needs.

Portability and Renewability

- Portability means you can switch from one insurer to another without losing benefits like waiting periods served.

- Renewability is the assurance that the Health Insurance Company can be renewed until a specified age or lifelong.

Many reputable insurers offer lifelong renewability and portability, which are important for long-term coverage.

Discounts and Loyalty Benefits

Some companies offer:

- No Claim Bonus (NCB): Reduced premiums for claim-free years.

- Family Floater Discounts: Lower premiums when covering the whole family under one plan.

- Senior Citizen Discounts: Health Insurance Company Special rates for older adults.

- Early bird discounts: Discounts when purchasing early in the year or during open enrollment.

Check which insurers provide such benefits to maximize your value.

The Importance of Reviews and Ratings

Third-party ratings from agencies like J.D. Power, AM Best, and local regulatory bodies provide insights into:

- Customer satisfaction

- Financial strength

- Claims service quality

- Market reputation

Reading both expert reports and consumer reviews gives you a balanced perspective on the company.

Tips for Buying Health Insurance Online

Online platforms make it easy to compare plans and buy instantly, but keep these tips in mind:

- Use trusted comparison websites with updated data.

- Double-check policy details on the insurer’s official site.

- Beware of policies with hidden costs or unclear clauses.

- Ensure secure payment gateways when making online purchases.

- Keep digital and physical copies of your policy documents.

Common Mistakes to Avoid When Choosing a Health Insurance Company

- Choosing the cheapest plan without checking coverage.

- Ignoring waiting periods and exclusions.

- Not verifying network hospitals in your area.

- Overlooking the insurer’s claim settlement track record.

- Forgetting to update the policy after life changes.

- Not reading policy documents thoroughly.

- Ignoring the importance of customer service responsiveness.

Avoiding these mistakes can save time, money, and frustration later.

Special Considerations for Senior Citizens

- Look for companies specializing in senior health insurance.

- Choose plans with lower deductibles and comprehensive coverage.

- Verify if the insurer covers pre-existing conditions and chronic illnesses.

- Check for easy claim processes and home healthcare services.

- Consider companies with good reputations for senior care.

The Impact of Government Regulations and Schemes

In many countries, governments regulate health insurance to protect consumers. Stay informed about:

- Government-mandated coverage minimums.

- Subsidies or tax benefits.

- Public health insurance options.

- New regulations affecting insurer operations.

An insurer compliant with government standards usually provides more security and peace of mind.

How to Compare Health Insurance Plans Effectively

With so many health insurance companies and plans available, it’s vital to compare them methodically to find the best fit. Here’s a step-by-step approach:

List Your Priorities

- Coverage needs: What treatments and conditions must be covered? For example, maternity, chronic illness, outpatient care.

- Budget: How much can you afford for premiums and out-of-pocket expenses?

- Preferred hospitals: Do your favorite doctors or hospitals fall under the insurer’s network?

- Additional benefits: Do you want wellness programs, mental health support, or international coverage?

Collect Policy Information

Gather detailed policy brochures or access insurer websites to review:

- Sum insured amounts

- Coverage inclusions and exclusions

- Waiting periods

- Premiums and deductible structures

- Co-payment terms

- Renewal conditions

Use Online Comparison Tools

Utilize comparison websites that let you enter your details and instantly view plans side-by-side. Features to check include:

- Premium vs coverage

- Network hospitals list

- Customer reviews and claim settlement ratios

- Policy benefits and riders

Check Reviews and Ratings

Look beyond price by researching customer satisfaction, complaint ratios, and regulatory authority ratings. These provide insight into claim settlement efficiency and service quality.

Calculate Total Cost of Ownership

Don’t just consider premiums. Factor in deductibles, co-payments, exclusions, and possible out-of-pocket costs during claims. Some low-premium plans might cost more overall.

Contact the Insurer for Clarifications

Before finalizing, call customer support to clarify any doubts, check response times, and evaluate service quality.

Understanding Common Health Insurance Terms

Familiarity with key terms can empower you to make smarter decisions:

- Premium: Regular payment to keep your policy active.

- Deductible: Amount you pay before insurer covers costs.

- Co-payment: Portion of claim amount paid by you.

- Sum insured: Maximum coverage amount per year or policy term.

- Exclusions: Conditions/treatments not covered.

- Network hospital: Hospitals where you can avail cashless treatment.

- Pre-existing condition: Illness or condition existing before policy start.

- Claim settlement ratio: Percentage of claims paid by insurer.

- Waiting period: Time before coverage starts on certain conditions.

- Portability: Option to switch insurer without losing benefits.

Understanding these helps avoid misunderstandings and hidden costs.

Also Read: What Does an Insurance Agency Do?

Conclusion

Selecting the right health insurance company requires careful consideration of various factors, including your healthcare needs, the insurer’s reliability, coverage options, and costs. By conducting thorough research and comparing different policies, you can make an informed decision that ensures comprehensive healthcare coverage for you and your family.

FAQs

- What is the Claim Settlement Ratio, and why is it important? The Claim Settlement Ratio (CSR) is the percentage of claims an insurer settles out of the total claims received. A higher CSR indicates the insurer’s reliability and efficiency in processing claims.

- How can I find out if my preferred hospital is in the insurer’s network? Insurers typically provide a list of network hospitals on their websites. You can also contact their customer service for this information.

- What does the waiting period mean in health insurance? The waiting period is the time you must wait before certain benefits, like coverage for pre-existing diseases or maternity, become active in your policy.

- Is it advisable to choose a policy with a high co-payment clause? While a high co-payment can reduce premiums, ensure you can afford the out-of-pocket expenses during a medical emergency.

- How often should I review my health insurance policy? It’s recommended to review your policy annually or after significant life events, like marriage or the birth of a child, to ensure it still meets your needs.

- Can I switch health insurance providers? Yes, you can switch providers, but ensure the new policy offers comparable or better coverage. Some insurers may offer portability options.

- Are there tax benefits associated with health insurance? In many countries, health insurance premiums qualify for tax deductions, reducing your taxable income.